|

|||

|

|

|

||

|---|---|---|

|

||

|

||

|

||

|

||

|

||

|

|

|

|

The Ultimate Guide to Conventional FHA Refinance: Everything You Need to KnowUnderstanding Conventional FHA RefinanceRefinancing a home loan is a significant decision that can impact your financial future. A conventional FHA refinance allows homeowners to replace their current Federal Housing Administration (FHA) loan with a conventional loan, or vice versa. This process can be beneficial for various reasons, including reducing interest rates or changing loan terms. Key Benefits

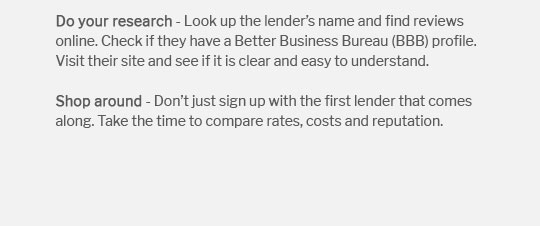

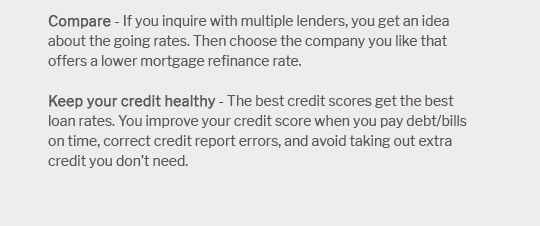

Steps to RefinanceEvaluate Your Financial GoalsBefore proceeding, it's crucial to assess your financial objectives. Are you looking to lower your monthly payments or pay off your loan faster? Understanding these goals will guide your refinancing decision. Check Your Credit ScoreA strong credit score can help you secure better terms. If necessary, take steps to improve your credit before applying. Shop Around for LendersIt's essential to compare offers from multiple lenders to find the best refi company that suits your needs. Look for competitive rates and favorable terms. Common ConsiderationsWhen refinancing, consider the costs involved, such as closing costs and any prepayment penalties. Additionally, consider the long-term savings versus the immediate expenses. Calculating SavingsUse online calculators to estimate potential savings. For instance, understanding 30 year cash out refinance rates can provide insights into how much you can save over time. FAQs about Conventional FHA RefinanceWhat is the difference between FHA and conventional loans?FHA loans are backed by the government and typically have more lenient credit requirements. Conventional loans, on the other hand, are not government-backed and usually require a higher credit score. Can I refinance an FHA loan to a conventional loan?Yes, refinancing from an FHA loan to a conventional loan is possible and can be beneficial in eliminating mortgage insurance and securing better interest rates. How do I qualify for a conventional loan?To qualify for a conventional loan, you typically need a good credit score, a stable income, and a debt-to-income ratio that meets the lender's requirements. What are the costs associated with refinancing?Refinancing costs can include appraisal fees, closing costs, and potentially prepayment penalties. It's important to compare these costs against potential savings. https://www.hud.gov/program_offices/housing/comp/premiums/ufrefi

Conventional Refinance: The prior loan was not FHA-insured and the new loan is being FHA-insured. This type of loan is processed the same as purchase cases for ... https://better.com/faq/refinancing-your-mortgage/can-a-borrower-refinance-from-another-loan-type-fha-va-usda-to-a

Yes, you can refinance a government loan such as an FHA, VA, or USDA loan to a conventional loan. Refinancing to a conventional loan can be an effective way to ... https://www.fha.com/fha_article?id=3416

You can financially qualify to refinance a conventional mortgage loan with an FHA loan. FHA loan guidelines say you can have credit scores in the 580 range or ...

|

|---|